Call: 470-202-8790

Toll Free: 855-882-9637

James F. Brown, Financial Strategist

Serving Our Clients Since 2003

Go Inside TFFL

Stretch IRA: Strategy for the Future

A Stretch IRA is a wealth-transfer strategy that allows you to extend the period of tax-deferred earnings on the assets of a pre-existing, or newly established IRA by passing your IRA assets to a younger beneficiary. This allows the money that would have been paid in taxes to work for your heirs, instead of Uncle Sam.

An article in Business Week, states an IRA beneficiary lost over 90% of his IRA due to immediate taxation. This could have been avoided had a proactive advisor been consulted.

Under IRS regulations issued in 2002, any individual who holds a traditional IRA can change the beneficiary to "stretch" IRA distributions. If you do not need to live on your IRA assets and want to benefit younger generations, consider using the Stretch IRA strategy.

A Stretch IRA provides tax-efficient wealth transfer.

- The law requires that once you reach age 70½, you must withdraw a required amount from your traditional IRA each year (RMD). When you choose to withdraw no more than those required distributions from your IRA and designate a younger beneficiary, you can extend the life of your IRA.

- Under the new IRS regulations, if you have an individual designated beneficiary, your beneficiary will not be required to completely withdraw your IRA assets either within five years of your death or over your remaining life expectancy. When a younger beneficiary inherits an IRA, the remaining balance can be paid out over the younger person's single life expectancy, effectively stretching out the length of time that withdrawals can be taken from that IRA. This extends the period of tax-deferred earnings of assets within an IRA beyond the lifetime of the person who set up the IRA.

- Payments to beneficiaries are paid out as income (RMD), which may not be subject to the 10% penalty tax even for a beneficiary under age 59½.

- Most of the Stretch IRA planning is revocable until death. So, for example, if your financial situation changes and you need more income in retirement, you can take larger IRA distributions as needed. However, once you reach age 70½, you can't request a smaller amount than your required minimum distributions.

- Similarly, if the beneficiary's situation changes after the death of the owner, he or she may take distributions exceeding the required minimum distributions.

- You can change your beneficiary at any time until death. In most cases, such a change would not affect the amount of required minimum distributions during your lifetime.

- It is important to know that you can only do a "Stretch IRA" if you have a willing custodian. If you do not know whether you have a "Stretch IRA" or not, you may want to consider a new advisor.

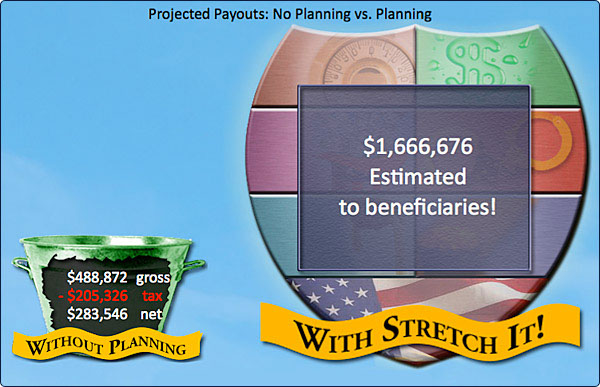

Stretch IRA - Example

Original IRA $250,000 Net to Heirs - Outcome Comparison

Numbers based on married couple of 65 and 64 with one beneficiary.

Without Planning

- Loss of tax deferral

- Lump sum of income tax

With Planning

- Maintain tax deferral

- Provide a lifetime of income for children and grandchildren

- Provides a Legacy for Grandparents

Understanding Roth IRA - The Roth IRA Conversion

When you choose to put money into an IRA, you make a deal with the government to pay taxes on it later, when you take the money out. If you choose a traditional IRA, it is tax-deferred and the taxes are deferred until withdrawal. Senator William Roth, Jr. (R-DE) introduced the IRA Expansion Bill on March 22, 1999. This new Roth IRA created was not tax-deferred, but presented the scenario upon which one would not pay taxes on the gains. A Roth IRA Conversion allows you to turn your traditional IRA into a Roth IRA, whereas you pay taxes up front on the converted amount, but NONE later. That means once you've created the Roth IRA, you don't have to worry about taxes upon withdrawal.

Determining when (or if) you should convert to a Roth IRA is an individual decision based on factors such as your financial situation, age, tax bracket, current assets and alternate sources of retirement income. Your unique circumstances help determine what is right for you.

Roth Frequently Asked Question #1: Can I convert my IRA or employer plan to a Roth IRA?

The answer is most likely, YES! In 2010, the restrictions for Roth IRA Conversions were greatly lifted and it has opened the door to allow many more people to convert to a Roth IRA. Call us today to find out how you can convert and mazimize your IRA.

Roth Frequently Asked Question #2: Can I name a trust as the beneficiary of my IRA or Roth IRA?

YES, you can name a trust as the beneficiary of your IRA or Roth IRA. However, do not do this unless you understand all of the ramifications of having a trust instead of an individual inheriting the IRA. Always consult with an IRA expert advisor before taking this step. Never move your IRA assets into the trust or retitle your IRA into the name of the trust. Both of those actions are taxable events and you will owe income tax on the entire balance in your IRA and you will no longer have an IRA!! The trust should simply be named as the beneficiary on the beneficiary form.

Here are two important links that serve as resources for your benefit:

Should you have any questions or need to learn more about how to leave a legacy, please contact us.

©2016 James Brown Financial Services. All Right Reserved. | Terms and Conditions | Privacy Policy

Conyers Office:

2890 GA Hwy 212, Suite A216 • Conyers, GA 30094

College Park Office:

3707 Main Street • College Park, GA 30337